Living in a Post Bretton Woods World

The rules change, but the game remains the same.

I believe in free trade – and 99.9% of the time, I would be dead set against tariffs – but you can only have a free trade based global market if everybody plays by the same rules. In today’s economic environment, tariffs may seem to be a blunt instrument to use, but with the hole our elected officials have dug for us, I’m not seeing many arrows left in the quiver.

We are boxed in.

After WWII, the Bretton Woods agreement created a platform for the post-WWII economic world to play by the same set of rules.

But we no longer live in the Bretton Woods world.

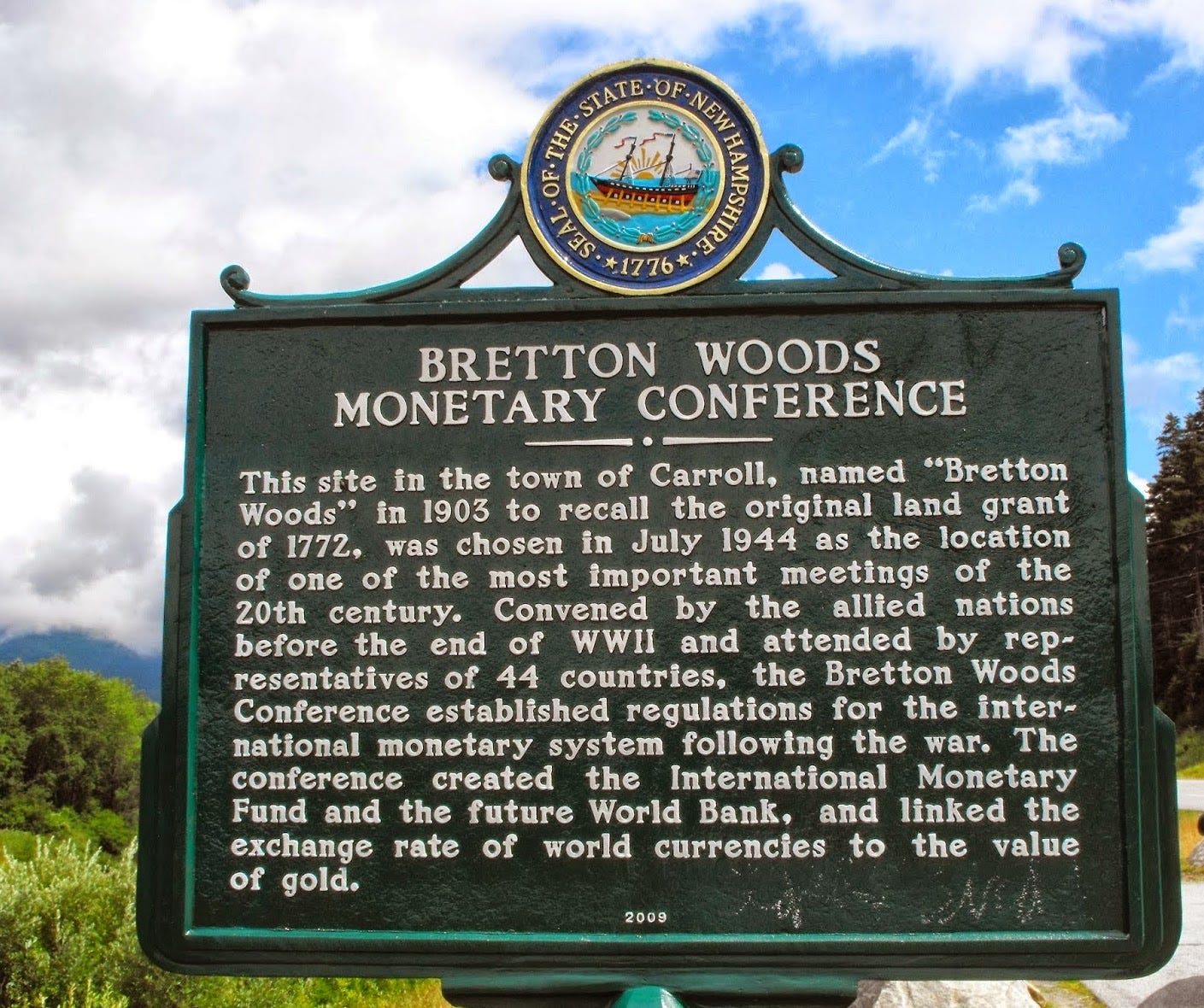

The Bretton Woods system, established in July 1944, was a bold attempt to reshape the global economy after the chaos of World War II. Convened in Bretton Woods, New Hampshire, the United Nations Monetary and Financial Conference brought together 44 Allied nations to forge a stable financial framework. The goal was clear: prevent the economic turmoil of the 1930s—marked by competitive currency devaluations and the Great Depression—from recurring. Led by British economist John Maynard Keynes and U.S. Treasury official Harry Dexter White, the conference birthed a system that would influence international finance for nearly three decades.

At its core, Bretton Woods established a fixed exchange rate regime. Currencies were pegged to the U.S. dollar, which was convertible to gold at $35 per ounce, making the dollar the linchpin of global trade. This structure relied on U.S. economic dominance, as America held about 75% of the world’s monetary gold in 1944. Countries agreed to keep their currencies within a 1% band of the dollar’s value, with adjustments allowed only in cases of "fundamental disequilibrium" and with approval from the newly created International Monetary Fund (IMF). The IMF provided loans to stabilize nations facing temporary deficits, while the World Bank, also born at Bretton Woods, focused on funding reconstruction and development.

The system reflected a compromise between competing visions. Keynes advocated for a supranational currency, "Bancor," to avoid dependence on any single nation, but the U.S., wielding its post-war might, insisted on a dollar-centric model. This decision paid off initially. The 1950s and 1960s, often dubbed the "Golden Age of Capitalism," saw unprecedented growth, as stable exchange rates fueled trade and investment. Western Europe and Japan rebuilt their economies, aided by Bretton Woods institutions and the U.S. Marshall Plan.

Yet, the system’s rigidity sowed the seeds of its downfall. By the late 1960s, U.S. trade deficits—driven by Vietnam War spending and domestic programs—flooded the world with dollars. Foreign nations, like France under Charles de Gaulle, began redeeming dollars for gold, straining U.S. reserves, which dropped from 20,000 tons in 1944 to 8,000 by 1971. Currency markets grew restless, speculating against the dollar’s fixed value. On August 15, 1971, President Richard Nixon delivered the "Nixon Shock," suspending dollar-to-gold convertibility. By 1973, the world shifted to floating exchange rates, ending Bretton Woods.

Some of the legacy of Bretton Woods endures.

The IMF and World Bank remain pillars of global finance, though their missions have evolved. The dollar, untethered from gold, still reigns as the world’s reserve currency - a remnant of its Bretton Woods primacy but the system’s collapse revealed the limits of fixed regimes in a dynamic world, but its successes, like fostering post-war recovery, are undeniable.

Bretton Woods was a rare moment of international unity, a grand experiment that stabilized the globe until its own weight pulled it apart, leaving lessons for today’s interconnected economy.

Bretton Woods was most certainly a boost for America’s economic interests – but it also made us, as the Democrats like to say when they want to spend more money, “a wealthy nation”. It also made us a de facto ATM for every nation in the world, a tool to assuage the left’s guilt for our prosperity – after they got their cut, of course.

I have been arguing about tariffs, not necessarily because I think they are peachy keen, but because it is something that we have not employed since 1930, when conditions were completely different.

Maybe they work, and I hope they do. Maybe they won’t. Many hope they don’t. What I do know is that, to paraphrase Einstein, doing what we have been doing and expecting a different result is the definition of insanity.

I’ve been leaning towards wait and see since Canadian politicians first started running around with their hair on fire screaming “Elbows up!” In the face of the tariff threat.

I get the imbalance, but I'm a big fan of Milton Friedman and am waiting to see if he or Trump is correct on this.

"Our tariffs hurt us as well as other countries. We would be benefited by dispensing with our tariffs even if other countries did not".

And I'm open to being wrong.